One of the key roles for a good mortgage adviser is to provide people on what makes a good home loan. There are other things that advisers do like arranging the home loan and getting competitive interest rates, but probably the most important role is to know what makes a good home loan for a persons individual situation.

You see, it’s much more important to have the right home loan than just a slightly lower interest rate.

Too often we see people choose their home loan on either:

- It’s the bank they already have bank accounts with

- It’s the first bank to approve their home loan

- It’s the bank advertising the lowest interest rates

Now we know that these might all seem like good reasons to choose a home loan and the banks might be happy enough that you consider these are the key things – but they are not.

You need to remember that a home loan is a large and long-term financial commitment, and therefore knowing what is a good home loan could be one of your best financial decisions – it can make your life easier, less stressful and save you a lot of money in the long term.

What makes a good home loan?

What’s defined as a good home loan may differ from person to person, but for a home loan in New Zealand you will want to split your mortgage into a minimum of two fixed loans and then have a small amount as a revolving credit. You should make sure that you can pay extra onto the fixed loans so that you can pay the loans off faster when you can, but without changing the underlying loan term as that can cause unwanted financial pressure when interest rates increase. The best home loans are provided by AIA Go Home Loans and TSB Bank who both offer fixed home loans that are very flexible and also are typically very competitive.

What do we mean when we say what makes a better home loan?

First let’s think about the reasons that you might use to choose a home loan, and then dive a little deeper into those reasons to see if they are really valid reasons.

Reason 1: Go To The Bank You Know

If you want a home loan then it seems like an easy option to approach the bank that you know. They have access to your banking records and already have you set up in the banks systems it can be quicker and even easier for them to assess your application and approve a home loan.

But how do you know that this bank offers the best option?

You probably don’t, but still many Kiwis are just happy to get their home loan approved. It’s common to hear people say that “their bank” has looked after them well, but have they really?

If you don’t know what makes a good home loan then it’s easy to just think that they are all basically the same, and the bank will probably not tell you any differently even if they did know what they had offered was not really that good. At best, the person at the bank will tell you about the features that the home loan they have can offer.

Sure, to most people it may seem quite good as there has been no real comparison.

Reason 2: The Bank That Approves Your Mortgage First

When you are buying a house you may get pressure from the real estate agent making you think that you may need your home loan approved as quickly as possible.

You are probably not even really focused on the home loan – instead you have fallen in love with the new home and will do whatever it takes to make sure that you can buy it.

This is especially the case for first home buyers.

Unfortunately we’ve seen that most people are happy to have an approval and will go with the bank that approved them first. That often means they miss out on a better home loan.

It’s really no different to any other industry – the banks that can offer the best home loan will generally be busier and therefore slower than a bank that has just an okay mortgage type.

It’s always best to try for the best home loan first and be prepared to wait a bit to get it approved.

Reason 3: The Bank That Advertises The Lowest Interest Rate

There is a reason that banks advertise a special interest rate, and it’s to get more “new” business.

Banks that offer special rates often pick a specific fixed loan term so they can lock borrowers in for that period, and they know that most people will then stay with the bank. When that fixed term ends most people will just refix again without taking much notice of the interest rate as long as it’s okay.

Knowing that you have the lowest rate seems important at the time, but no bank will always have the lowest interest rates.

It’s more important to know that the bank you are with will consistently have competitive home loan rates across the range of fixed terms that are offered. Remember that most people will have home loans for many years and so you want to know that you get good rates most of the time.

If you are using a mortgage adviser to refix your interest rates then they should also be making sure that they keep the bank honest and see if they can get the bank to match any lower rates that may be being offered.

You are welcome to contact me and I do this for free regardless if I arranged the home loan for you or not.

In New Zealand we have a number of banks that offer similar home loan interest which some offering special discounted rates at times.

Bank of China generally offers the lowest home loan interest rates, but the loans are not as flexible as some other banks. TSB Bank is a New Zealand owned bank and generally offers a very competitive home loan interest rate trying always to remain lower than the big four Australian owned banks; ANZ, ASB, BNZ and Westpac.

What Should You Consider With Your Mortgage?

A home loan is a large financial commitment and it’s generally something that you will have for a long time too.

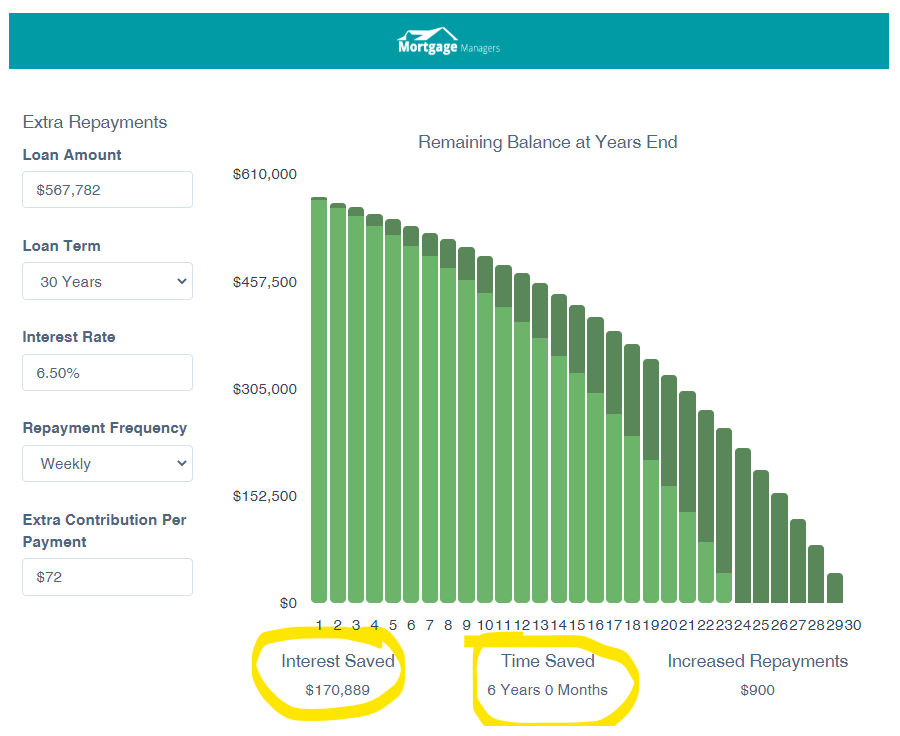

Often a home loan will be a families biggest financial commitment and the average mortgage in New Zealand was reported to be $362,553 and with first home buyers that was higher at $567,782 (Canstar – January 2023)

Those are big numbers, but what shocks most people is how much they will end up paying for the mortgage over the lifetime of the loan.

Example: Average First Home Buyer $567,782 (30-Years @ 6.50%)

If you are a first home buyer and have the average home loan ($567,782) then using the interest rate of 6.50% means that your weekly repayments would be $828 and over the 30-years you would pay the bank a total of $1,291,348

The bank are going to make a lot of money from having you as a home loan customer, and that’s before you use any other bank products.

We would prefer that the banks do not make quite as much and as the graph below shows, if you can increase your repayments by just $72 a week you will pay your home loan off 6-years faster and save over $170,000.

It makes sense to have a mortgage that allows you to pay your mortgage off faster as this is what really saves you money.

We believe that everyone with a home loan should have this explained to them and they should make sure that they have regular meetings or discussions to ensure that they are not paying the bank too much.

- Will your bank show you how to pay them less? Highly unlikely!

- Will your mortgage adviser show you how to save money? Maybe some do, but that’s exactly what we do.

- Just using a bank that that you know and feel comfortable is not going to mean that you have the best home loan as that bank may not have access to those key features.

- Just using the bank that approved you fastest will probably not show you how to save what you pay the bank, as it’s unlikely that they have the best mortgage – otherwise they would be too busy to be the fastest.

- Just going to the bank that had the lowest interest rate it can look okay in the first year or two, but generally banks offer special rates when they need more business ands those good interest rates rarely last.

The best home loan will be one that offers flexibility so that you can manage the loans as your circumstances change over time and yet gives you the ability to pay the loans off faster in those periods when you can.

Let’s Consider The Key Features Of A Good Home Loan

When trying to establish what is the best home loan you should consider what you want, and for the purposes of this article we will assume that you want to be able to pay it off as fast as you can, save a huge amount and have the flexibility to change the home loan to suit life’s changes.

We are specifically talking about a home loan here.

A mortgage on an investment property or where the mortgage is used for business may be different as you may never plan to have the property or mortgage for too long. We are also not talking about bridging finance or when specialist finance is needed.

So here are the key features that a good home loan should have:

- Revolving Credit Facility – when used properly these can be used as the main loan funding facility. It does not need to have a large limit, but it gives you the control of the loans and flexibility to adjust the repayments, the ability to save a fund lump-sum repayments and also to build up a back-stop. These facilities are great for pre-planning for a change in your financial situation like starting a family, returning to education or training and a change in jobs or careers.

- Fixed Home Loans – the interest rates are almost always lower on a fixed home loan and the nature of being “fixed” gives the comfort and ability to budget. Most people want to have most of their lending on fixed rates for these reasons and it’s always best to split up your mortgage into two, three or more fixed loans too as that gives added flexibility.

- Ability to Increase Repayments – with all home loans you can increase the repayments when your loans are at the floating rate (higher rate) but there are less options when you select a fixed rate. Almost all banks allow you to increase your repayments on fixed loans, but many are quite limited. Some will limit you to ‘say’ 5% of the total mortgage, or $15,000 per year but what you want is a mortgage type that allows you to increase each loan by ‘say’ $1,000 a month so if you have your mortgage split into five loans you have five opportunities to increase the repayments to a total of $5,000 a month extra which is $60,000 per year.

- Increase Repayments Without Shortening Loan Terms – unfortunately with most banks when you increase any repayments by default the bank shorten the loan term. This sounds fine at first, but a mortgage is a long-term commitment and things will change over time so you will not want to be forced into a situation when you need to make larger repayment’s because of this. Specifically if interest rates increase, or your income reduces – both of these are quite common and cause a lot of issues.

- Ability to Decrease Repayments – while it’s good to be able to increase repayments on a fixed loan, having the ability to decrease the repayments as well gives people the confidence to do increases beyond what they may have done otherwise. This alone can mean you will end up doing larger increases and therefore save more.

The banks have other features too that they promote, and some are useful too. The features listed here are the main and arguably the most important features that will help you save the most on your mortgage.

Talk to me, if you already have a home loan and it’s not as good as it could be then I can help arrange to refinance you so that you benefit from a better home loan, and it will also cost you nothing as the banks pay us to do this.